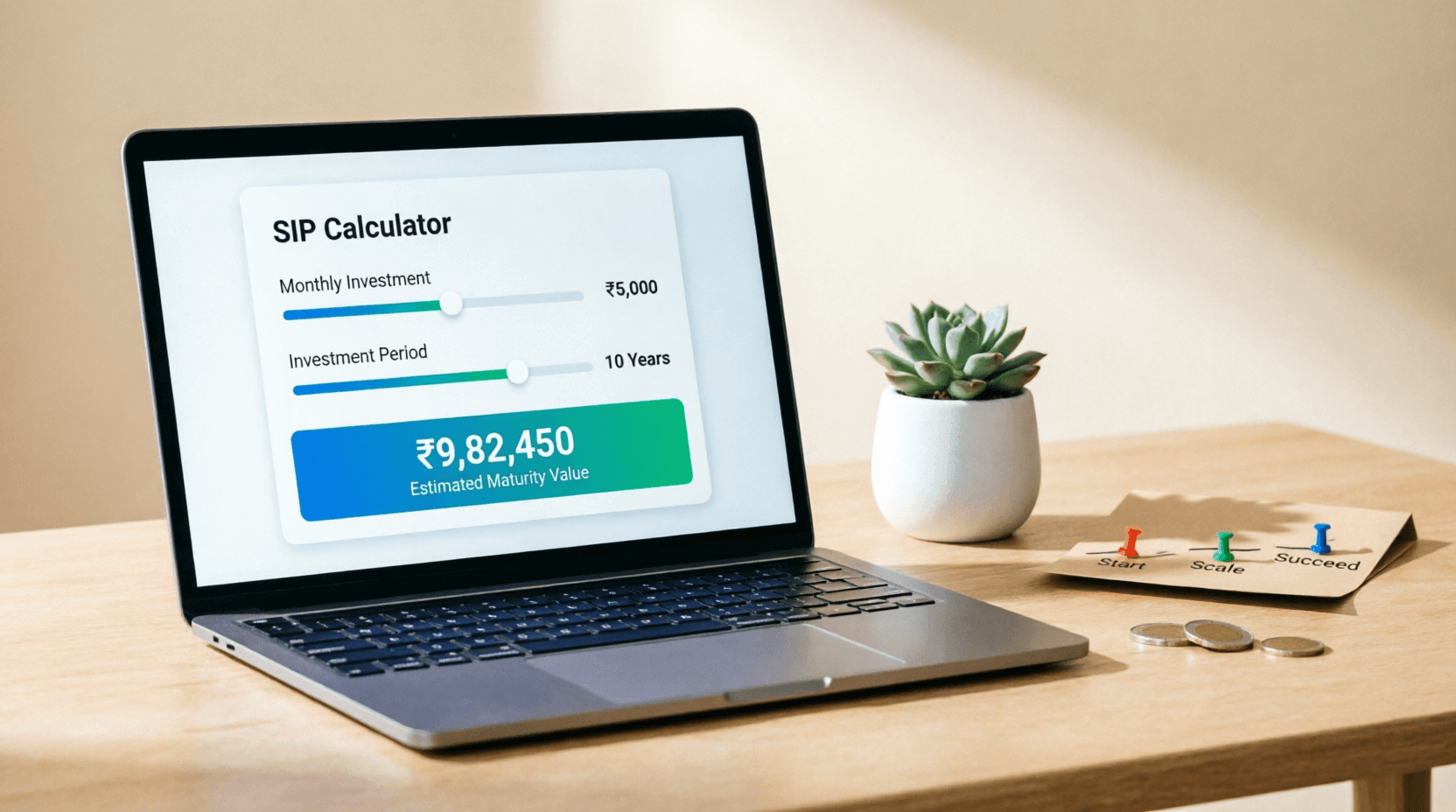

Instead of guessing or wrestling with confusing spreadsheets, you can get a clear, instant answer in under 30 seconds. That’s exactly what this SIP calculator is built for.

What This Tool Actually Does

At its core, this is a planning assistant disguised as a simple web tool. You tell it three things:

- How much you can comfortably set aside every month

- What kind of annual return you realistically expect

- How long you plan to keep investing

In return, it gives you three numbers that actually matter:

- Total Invested: The hard cash you put in

- Estimated Returns: The growth your money earns over time

- Total Value: What you’ll likely walk away with

No jargon. No hidden assumptions. Just a clean breakdown that shows exactly where your money is heading.

How It Works (Step-by-Step)

The interface is intentionally straightforward. Here’s how to use it:

- Set your monthly investment

Use the slider or type directly into the box. Even ₹1,000 counts. The tool instantly updates as you adjust. - Pick an expected annual return rate

Slide to your target percentage. If you’re investing in equity mutual funds, 10–12% is a historically reasonable long-term estimate. For debt or hybrid funds, 6–8% makes more sense. - Choose your investment period

Drag the slider to match your goal timeline. Short-term (1–3 years), medium (5–7 years), or long-term (10+ years). - Read the results

The calculator instantly shows your total value, splits it into “Invested” (blue) and “Returns” (green), and displays a visual bar so you can see how much of your wealth comes from compounding versus your own contributions.

Tweak any number, and everything recalculates in real time. It’s that simple.

Key Features & Why They Matter

- Instant visual breakdown – The color-coded bar removes guesswork. You immediately see how much of your future corpus is pure growth.

- Real-time adjustments – Slide the monthly amount or years to see how small changes create massive differences over time.

- Zero login, zero clutter – No pop-ups, no email traps. Just open, calculate, and move on.

- Goal-aligned planning – Works for vacations, down payments, education, retirement, or emergency buffers.

- Beginner-friendly, pro-approved – Simple enough for first-time investors, yet accurate enough for seasoned portfolio planners.

Real-Life Scenarios Where This Shines

Scenario 1: The First Job SIP

Arjun just landed his first role and can spare ₹6,000/month. He’s eyeing a master’s degree abroad in 7 years. Plugging ₹6,000 at 12% for 7 years shows ~₹7.8 lakhs. He realizes he’ll need to bump it to ₹8,500 or extend the timeline slightly. The calculator just saved him from under-saving.

Scenario 2: The “Late Starter” Check

Meera, 38, worries she started investing too late. She tests ₹10,000/month for 15 years. The result? ~₹48 lakhs. She sees that consistency still wins, even if she missed her 20s. The tool gives her a clear baseline to adjust her budget.

Scenario 3: Side-Hustle Buffer

Rohan earns an extra ₹4,000/month from freelancing. He wonders if parking it in a SIP is worth it. At 10% over 5 years, it grows to ~₹3.1 lakhs. He decides it’s perfect for a travel fund, not just “savings.”

Why This Calculator Beats the Alternatives

Many financial sites bury SIP calculators behind signup walls or overload them with complex charts you don’t need. Others use outdated return assumptions that paint an unrealistic picture.

This one stays lean. It doesn’t promise moonshots. It doesn’t ask for your phone number. It just runs the math transparently so you can make a decision today, not next week. Plus, the split between invested capital and earned returns helps you appreciate compounding without hype.

Tips to Get the Most Out of It

- Keep return expectations grounded. Equity markets don’t give 15% every year. 10–12% long-term is a safer planning baseline.

- Factor in inflation mentally. ₹10 lakhs in 2034 won’t buy what ₹10 lakhs buys today. Aim 3–5% higher than your actual target to stay ahead.

- Run “step-up” scenarios. Even increasing your SIP by 10% yearly dramatically boosts the final corpus. Try it in the calculator.

- Use it as a compass, not a guarantee. Markets fluctuate. The tool shows probable outcomes based on consistent investing, not fixed deposits.

- Revisit annually. Life changes, salaries change, goals shift. Update the numbers once a year to stay on track.

Frequently Asked Questions

1. Are the returns shown guaranteed?

No. Mutual fund SIPs are market-linked. The calculator uses your chosen return rate to project a likely outcome, but actual results will vary with market performance.

2. Does this calculator account for taxes?

It shows pre-tax projections. Depending on the fund type and holding period, capital gains tax may apply. Consult a tax advisor for post-tax planning.

3. What’s a realistic annual return to enter?

For long-term equity SIPs, 10–12% is widely used by financial planners. For debt or balanced funds, 6–8% is more appropriate.

4. Can I use this for goals under 3 years?

You can run the numbers, but short-term goals are better suited to liquid funds, recurring deposits, or fixed income instruments where capital preservation matters more than growth.

5. How often should I check my SIP projections?

Once a year is usually enough. Revisit it whenever you get a salary hike, change jobs, or adjust a major life goal.

Ready to See Your Numbers?

Plug in your monthly amount, pick a realistic return rate, and watch how time turns small, consistent steps into serious wealth. If the result excites you, you already know what to do next. If it falls short of your goal, now you know exactly how much to adjust. Either way, you’re planning with clarity instead of guesswork.

Try the calculator, tweak the sliders, and let the numbers guide your next move. Your future self will thank you for starting today.

💬 Comments (0)

No comments yet. Be the first to share your thoughts!

Leave a Comment