Introduction: That Small Interest Rate Difference is Costing You Big Money

Picture this: You're buying your first home in Austin, Texas. Two lenders approve your mortgage application for $250,000. Lender A offers 6.5% interest, Lender B offers 7%.

Half a percent doesn't sound like much, right?

Wrong.

Over 20 years, that tiny 0.5% difference will cost you an extra $17,760. That's enough to buy a reliable used car, fund your child's college savings, or take multiple family vacations.

Here's the thing: most Americans don't realize how much they're overpaying because they never compare loan offers properly. They look at the monthly payment, nod politely, and sign on the dotted line.

But what if you could see the entire picture before committing? What if you could instantly compare multiple loan offers side-by-side and know exactly which one saves you money?

That's where a Loan Comparison Calculator changes everything.

What Exactly is a Loan Comparison Calculator?

Think of it as your personal financial detective.

A loan comparison calculator lets you pit different loan offers against each other to see which one truly costs less—not just this month, but over the entire loan period.

Instead of juggling multiple calculators or drowning in Excel sheets, you enter details for Loan A and Loan B (or more), and the tool instantly shows you:

- Monthly payment for each option

- Total interest you'll pay over the years

- Total repayment amount

- The actual savings difference

- Interest as a percentage of principal

It's like having a side-by-side showdown between lenders, where the cheapest loan wins.

According to research from Freddie Mac, comparing loan offers from multiple lenders can save borrowers over $1,000 per year. And honestly, who wouldn't want that?

How Does It Work? (No Math Degree Required!)

Using a loan comparison calculator is ridiculously simple. Here's a step-by-step breakdown:

Step 1: Enter Loan A Details

Let's say you're comparing two mortgage offers for your dream home:

- Loan Amount: $250,000

- Interest Rate: 6.5% per year

- Tenure: 20 years

Step 2: Enter Loan B Details

Now input the second offer:

- Loan Amount: $250,000 (same amount)

- Interest Rate: 7.0% per year

- Tenure: 20 years

Step 3: Hit Compare and Watch the Magic

The calculator instantly crunches the numbers and shows you:

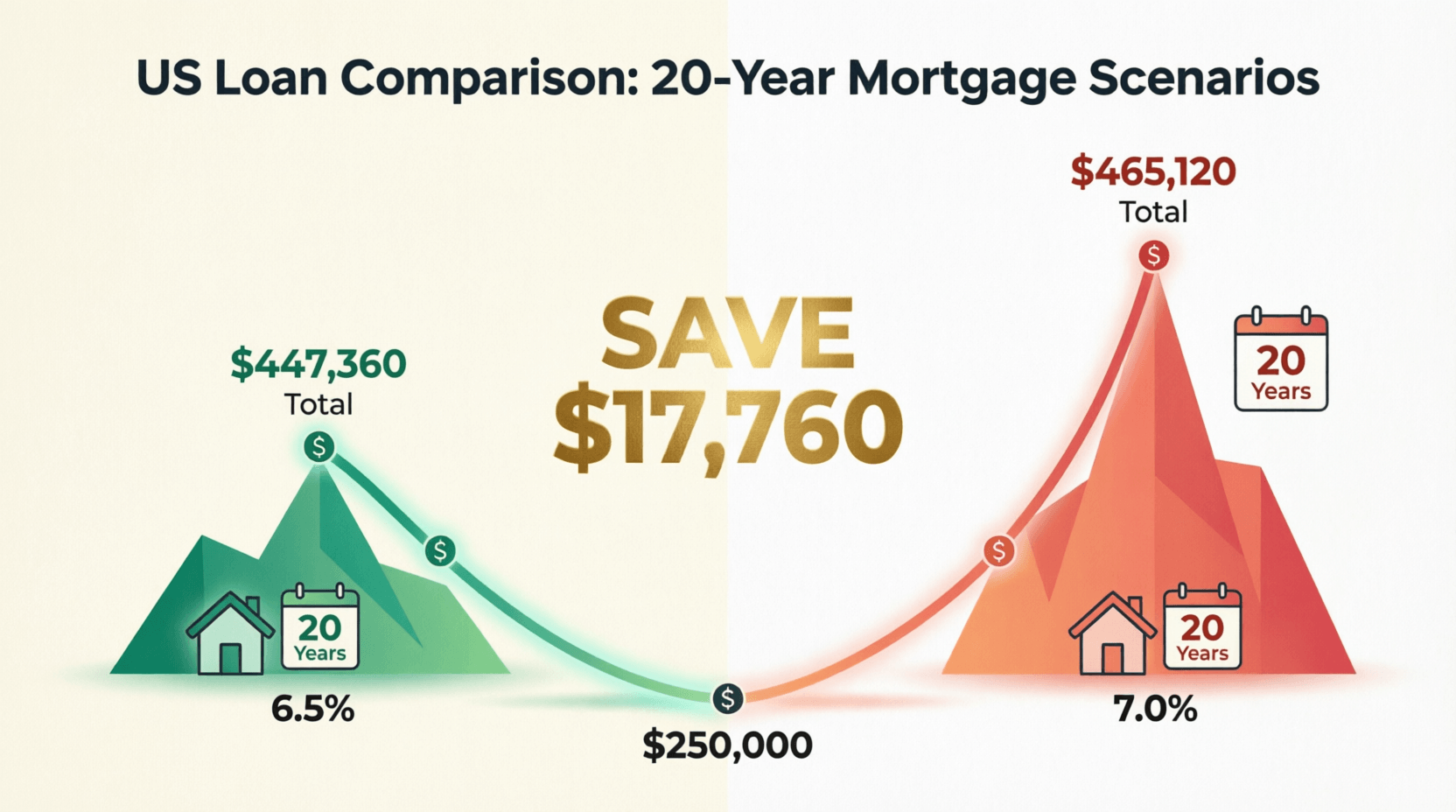

Loan A Results:

- Monthly Payment: $1,864

- Total Interest: $197,360

- Total Repayment: $447,360

- Interest as % of Principal: 78.9%

Loan B Results:

- Monthly Payment: $1,938

- Total Interest: $215,120

- Total Repayment: $465,120

- Interest as % of Principal: 86.0%

The Verdict: Loan A saves you $17,760 over the loan tenure.

That's it. No formulas, no confusion, just clear numbers that help you make a smarter decision.

Why This Tool is a Game-Changer (Key Features & Benefits)

1. See the Real Cost, Not Just Monthly Payment

Most borrowers focus only on the monthly payment. But here's what lenders don't highlight: a slightly lower payment with a longer tenure can actually cost you more in total interest. This calculator shows you the complete picture.

2. Instant Side-by-Side Comparison

Instead of opening five different tabs or calling each bank for calculations, you get everything on one screen. Clean, clear, and easy to understand.

3. Understand Interest Impact

Ever wondered how much of your payment actually goes toward interest? The "Interest as % of Principal" metric is eye-opening. In our example, you're paying nearly 80% of the loan amount in interest alone!

4. Negotiate Better Deals

Armed with concrete numbers, you can walk into a bank and say, "Lender A is offering me 6.5%. Can you beat that?" Suddenly, you're not just another customer—you're an informed borrower.

5. Plan for Different Scenarios

What if you reduce the loan term by 5 years? What if you increase your down payment? Play with different combinations to find your sweet spot.

6. Completely Free and Fast

Most online loan comparison tools are free to use and give instant results. No registration, no spam calls, just pure value.

Real-Life Scenarios: When This Tool Saves Your Wallet

Scenario 1: The Home Loan Hunt

Meet Sarah and Mike, a young couple looking to buy their first home in Denver, Colorado. They get loan quotes from three lenders:

- Wells Fargo: 6.75% for $320,000, 30 years

- Chase: 6.50% for $320,000, 30 years

- Quicken Loans: 7.00% for $320,000, 30 years

Using the comparison calculator, they discover Chase saves them $28,800 compared to Quicken Loans over the life of the loan. That's their entire kitchen renovation budget!

Scenario 2: The Car Loan Confusion

James wants to buy a $32,000 Tesla Model 3. The dealership offers financing at 7.9% for 7 years. His credit union offers 6.5% for 5 years.

The dealer's payment looks lower ($492 vs $625), but when he compares the total cost:

- Dealer loan: $41,328 total repayment

- Credit union loan: $37,500 total repayment

Savings: $3,828 by choosing the credit union loan, even with higher monthly payments.

Scenario 3: The Personal Loan Trap

Amanda needs $15,000 for her daughter's wedding. She gets two offers:

- Offer A: 8.99% for 3 years

- Offer B: 10.5% for 5 years

Offer B has a lower monthly payment, but the calculator reveals Offer A saves $2,340 in total interest. Sometimes a higher payment is actually smarter.

Scenario 4: The Refinance Decision

Robert and Lisa in Phoenix, Arizona are considering refinancing their mortgage. Their current loan:

- Current rate: 7.5% on $280,000 remaining, 25 years left

- New offer: 6.5% on $280,000, 25 years

The calculator shows they'd save $42,000 over the life of the loan—enough to fully fund their retirement accounts for two years.

Why This Calculator Beats Manual Calculations (and Other Tools)

Let's be honest—you could calculate everything manually using the payment formula, but do you really want to spend your evening wrestling with exponents and fractions? I didn't think so.

Here's what makes a good loan comparison calculator stand out:

✓ Accuracy You Can Trust

No human error. The tool uses standardized formulas to give you precise calculations every single time.

✓ Time-Saving

What takes 30 minutes manually happens in 30 seconds.

✓ Visual Clarity

Numbers are presented in an easy-to-read format with clear verdicts. No squinting at spreadsheets.

✓ Multiple Loan Comparison

Some advanced tools let you compare 3-4 loans simultaneously, not just two.

✓ No Registration Hassle

The best calculators don't ask for your phone number or email. Just calculate and go.

Pro Tips: How to Use This Tool Like a Financial Expert

Tip 1: Compare Total Cost, Not Just Payment

A lower monthly payment feels good today, but a lower total cost feels better over time. Always check the "Total Repayment" figure.

Tip 2: Play with Loan Terms

Try reducing the loan term by 5 years. Yes, your payment goes up, but your total interest drops significantly. Find a balance you're comfortable with.

Tip 3: Factor in Closing Costs

Some calculators let you add closing costs and other fees. A loan with 6.5% interest but $5,000 in closing costs might cost more than one with 6.75% interest and zero fees.

Tip 4: Check Prepayment Penalties

If you plan to make extra payments, choose a loan with no prepayment penalties. This isn't always in the calculator, but it's worth asking lenders.

Tip 5: Use Real Numbers

Don't estimate. Use the exact interest rate, term, and loan amount from your Loan Estimate forms. Even 0.25% makes a difference.

Tip 6: Compare at Least 3 Offers

Don't settle for comparing just two loans. Get quotes from 3-4 lenders. You might be surprised by the variation.

Tip 7: Revisit Before Closing

Interest rates change. If you're shopping for a loan over several weeks, recalculate before signing. That 7% offer might have dropped to 6.75%.

Tip 8: Consider Your Credit Score

Check your credit score before applying. Someone with a 760+ score could save tens of thousands compared to someone with a 640 score on the same loan amount.

Frequently Asked Questions (FAQs)

Q1: Is a 0.5% interest rate difference really worth comparing?

Absolutely! As we saw in the example, a 0.5% difference on a $250,000 loan over 20 years saves you $17,760. That's real money that could go toward your retirement, your kids' education, or your dream vacation.

Q2: Can I use this calculator for all types of loans?

Yes! Whether it's a mortgage, auto loan, personal loan, or student loan, the calculator works for any loan with a fixed interest rate and regular payments.

Q3: What if my loan has an adjustable interest rate?

Most mortgages have fixed rates, but if you're considering an ARM (Adjustable-Rate Mortgage), use the initial rate for comparison. Keep in mind that your actual payment might change if rates fluctuate. It's still useful for comparing initial offers.

Q4: Does this calculator include closing costs and other fees?

Basic calculators show interest and payments only. Some advanced versions let you add closing costs, origination fees, and other charges. Always ask lenders about hidden costs separately and factor them into your decision.

Q5: How many loan offers should I compare?

Ideally, compare at least 3-4 offers from different banks, credit unions, and online lenders. This gives you a better sense of the market and stronger negotiating power.

Q6: Will using this calculator affect my credit score?

No. Simply calculating and comparing loans doesn't impact your credit score. However, when you formally apply and the lender does a hard credit inquiry, that gets recorded. Multiple mortgage inquiries within a 45-day window typically count as a single inquiry for scoring purposes.

Q7: What's the difference between APR and interest rate?

Great question! The interest rate is what you pay to borrow the money. The APR (Annual Percentage Rate) includes the interest rate PLUS other fees and costs. Always compare APRs when shopping for loans—it gives you the true cost of borrowing.

The Bottom Line: Stop Guessing, Start Comparing

Here's what I've learned after years of writing about personal finance: the smallest financial decisions compound into the biggest outcomes.

Choosing the right loan isn't just about getting approved. It's about knowing you made the smartest choice for your future self.

That $17,760 you save by picking the better loan? You could:

- Invest it in a low-cost index fund and watch it grow

- Contribute to your 401(k) or IRA

- Build your emergency fund to 6 months of expenses

- Pay for your child's college textbooks and supplies

- Take that cross-country road trip you've been dreaming about

- Make extra principal payments to pay off your loan even faster

The choice is yours.

So next time you're shopping for a loan—whether it's for a home in Seattle, a car in Miami, or anything in between—don't just grab the first offer. Take 10 minutes. Use a loan comparison calculator. See the real numbers.

Your future self will thank you.

Ready to make a smarter borrowing decision? Try our free Loan Comparison Calculator today and discover how much you could save. Because when it comes to your hard-earned money, every dollar counts.

💬 Comments (0)

No comments yet. Be the first to share your thoughts!

Leave a Comment