Ever stood at the crossroads of a big financial decision, staring at a home loan or car loan offer, wondering: "Can I actually afford this?"

You're not alone. Last month, my friend Rahul almost signed up for a ₹50 lakh home loan thinking he could handle the payments. One look at the EMI breakdown later, he realized he'd be paying nearly ₹48 lakh in interest alone over 20 years. That's almost another house!

This is exactly why you need a reliable EMI calculator in your corner before making any borrowing decision.

What Exactly Is an EMI Calculator?

Think of an EMI calculator as your financial crystal ball. It's a simple online tool that tells you exactly how much you'll pay every month for your loan – no surprises, no guesswork.

An EMI (Equated Monthly Installment) calculator works by factoring in the loan amount, interest rate, and loan tenure to determine your monthly payments

Instead of wrestling with complex formulas, you just slide a few buttons and boom – instant clarity.

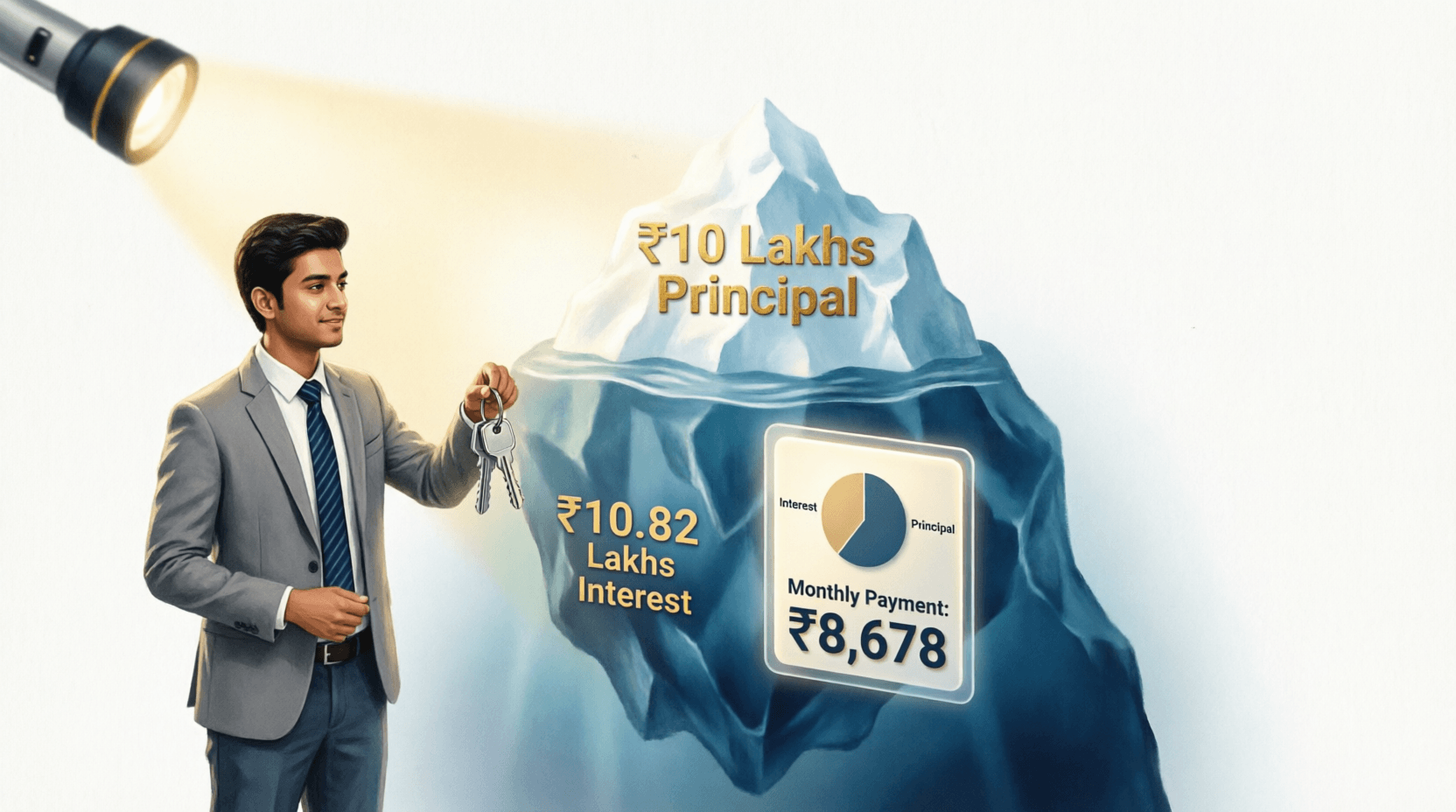

The calculator shown above does something even better: it breaks down exactly how much of your money goes toward the actual loan (principal) versus how much disappears as interest. That pie chart showing "52% int."? That's your wake-up call.

How Does It Work? (No Math Degree Required)

Using this tool is ridiculously simple. Here's the step-by-step:

Step 1: Enter Your Loan Amount

This is the total money you want to borrow. In our example, it's ₹10,00,000 (10 lakhs). You can adjust this using the slider or type it directly.

Step 2: Set the Interest Rate

Banks quote this as a yearly percentage. Our example shows 8.5% per annum, which is pretty standard for home loans in India right now.

Step 3: Choose Your Loan Tenure

How long do you want to repay? The example shows 20 years. Remember: longer tenure means lower monthly EMI but higher total interest.

Step 4: Hit Calculate (It's Automatic)

The tool instantly shows you:

- Monthly EMI: ₹8,678 – what leaves your account every month

- Principal Amount: ₹10,00,000 – the actual loan you took

- Total Interest: ₹10,82,776 – what you're paying extra

- Total Payable: ₹20,82,776 – the real cost of your loan

That last number is the eye-opener, isn't it? You're paying back double what you borrowed!

Why This Calculator Is a Game-Changer

1. Visual Breakdown That Makes Sense

That donut chart isn't just pretty – it's powerful. Seeing that 52% of your payment goes toward interest (not the actual loan) hits differently than just reading numbers. It's the difference between someone telling you "you'll pay a lot of interest" versus showing you half your money vanishes.

2. Real-Time Adjustments

Move any slider and watch everything update instantly. Want to see what happens if you increase your EMI by reducing the tenure from 20 to 15 years? Just drag the slider. The calculator uses the standard EMI formula: EMI = [P × R × (1+R)^N] / [(1+R)^N-1], but you don't need to know that

3. Year-Wise Schedule

The "Show Year-wise Schedule" button is pure gold. It reveals exactly how much principal and interest you pay each year. In the early years, most of your EMI goes toward interest – this schedule shows you the exact breakdown.

4. No Registration, No Spam

Unlike many financial tools that demand your email before showing results, this one respects your time. Calculate freely, experiment endlessly.

Real-Life Scenarios Where This Saves You

Scenario 1: The Home Loan Dilemma

Priya and Amit found their dream apartment – ₹60 lakhs. They have ₹15 lakhs for down payment, so they need a ₹45 lakh loan.

Using the calculator:

- At 8.5% for 20 years: EMI = ₹39,051, Total Interest = ₹48.72 lakhs

- At 8.5% for 15 years: EMI = ₹44,236, Total Interest = ₹34.62 lakhs

The insight: Paying ₹5,185 more monthly saves them ₹14.10 lakhs in interest. That's a family vacation every year for 15 years!

Scenario 2: The Car Loan Trap

Rohan wants a ₹12 lakh car. The dealer offers:

- Option A: 7 years at 9% interest

- Option B: 5 years at 8.5% interest

The calculator reveals Option B costs ₹1.42 lakhs less overall, even though monthly payments are higher. Without this tool, Rohan might've chosen the "lower EMI" trap.

Scenario 3: Prepayment Planning

You're 5 years into a 20-year home loan. Should you make a prepayment? The year-wise schedule shows exactly how much principal remains and how much interest you'll save by paying early.

Why This Tool Beats Manual Calculations

Let's be honest – you could calculate EMI manually using the formula

. But here's why you won't:

- Time: Manual calculation takes 10-15 minutes per scenario. This tool? 10 seconds.

- Accuracy: One wrong exponent in the formula and your entire plan is off.

- Comparison: Want to compare 3 different loan offers? That's 45 minutes of math versus 30 seconds of slider adjustments.

- Understanding: The visual pie chart and breakdown make abstract numbers concrete.

As one financial planner put it: "The best financial decision is an informed one. This tool removes the guesswork."

Pro Tips to Get Maximum Value

1. Play the "What-If" Game Don't just calculate once. Try different combinations:

- What if I borrow ₹8 lakhs instead of ₹10 lakhs?

- What if I negotiate the rate down to 8%?

- What if I repay in 15 years instead of 20?

2. Use the 40% Rule Financial experts suggest your total EMIs shouldn't exceed 40% of your monthly income

If the calculator shows ₹30,000 EMI, ensure your income is at least ₹75,000.

3. Check the Interest-to-Principal Ratio If the pie chart shows interest above 50% (like our example), consider:

- Increasing your down payment

- Choosing a shorter tenure

- Looking for better interest rates

4. Plan for Rate Changes If you're taking a floating-rate loan, calculate at 1% higher than the current rate. This prepares you for potential hikes.

5. Use the Year-Wise Schedule Strategically The schedule shows that in early years, most EMI goes to interest. This is why prepaying in the first 5 years saves maximum interest

Frequently Asked Questions

Q1: Is EMI calculator 100% accurate?

The calculation is mathematically precise based on the inputs you provide. However, actual EMIs may vary slightly if your bank uses different compounding methods or adds processing fees. Always confirm final numbers with your lender, but use this tool for solid estimates.

Q2: Can I use this for all types of loans?

Absolutely! Whether it's a home loan, car loan, personal loan, or even education loan, the EMI calculation formula remains the same

Just adjust the interest rate and tenure according to your loan type.

Q3: Why does my EMI stay the same even though I'm paying off principal?

That's how EMIs work – they're "equated" or fixed throughout the loan tenure. In early months, most of your EMI goes toward interest; later, more goes toward principal. The year-wise schedule shows this shift clearly.

Q4: Should I choose lower EMI or shorter tenure?

If you can afford higher EMIs, always choose shorter tenure. For example, a ₹10 lakh loan at 8.5%:

- 20 years: EMI ₹8,678, Total Interest ₹10.82 lakhs

- 15 years: EMI ₹9,847, Total Interest ₹7.72 lakhs

Paying ₹1,169 more monthly saves ₹3.10 lakhs overall.

Q5: How does prepayment affect my EMI?

Most calculators show standard EMI without prepayment. If you plan to prepay, you have two options: reduce your EMI amount or reduce your loan tenure. The year-wise schedule helps you model this.

The Bottom Line

Taking a loan without using an EMI calculator is like buying a house without checking the blueprint – possible, but risky.

The tool you see above transforms confusing financial jargon into clear, actionable insights. That ₹10 lakh loan isn't just ₹10 lakh – it's ₹20.82 lakhs over 20 years. Knowing this upfront changes everything.

Ready to make smarter borrowing decisions? Bookmark this calculator. Play with the numbers. Test different scenarios. Your future self will thank you when you avoid that ₹5 lakh interest trap or discover you can afford that home loan after all.

Remember: the best loan is an informed loan. Calculate first, commit second.

💬 Comments (0)

No comments yet. Be the first to share your thoughts!

Leave a Comment